Gold Outlook 2026: Why Gold May Stay Range-Bound in H2

Gold had every reason to rally in 2026.

War. Inflation. Rate uncertainty. Rising US debt risk. Geopolitical chaos.

On paper, this looked like the perfect setup for the world’s most famous safe-haven asset. But the market had other plans.

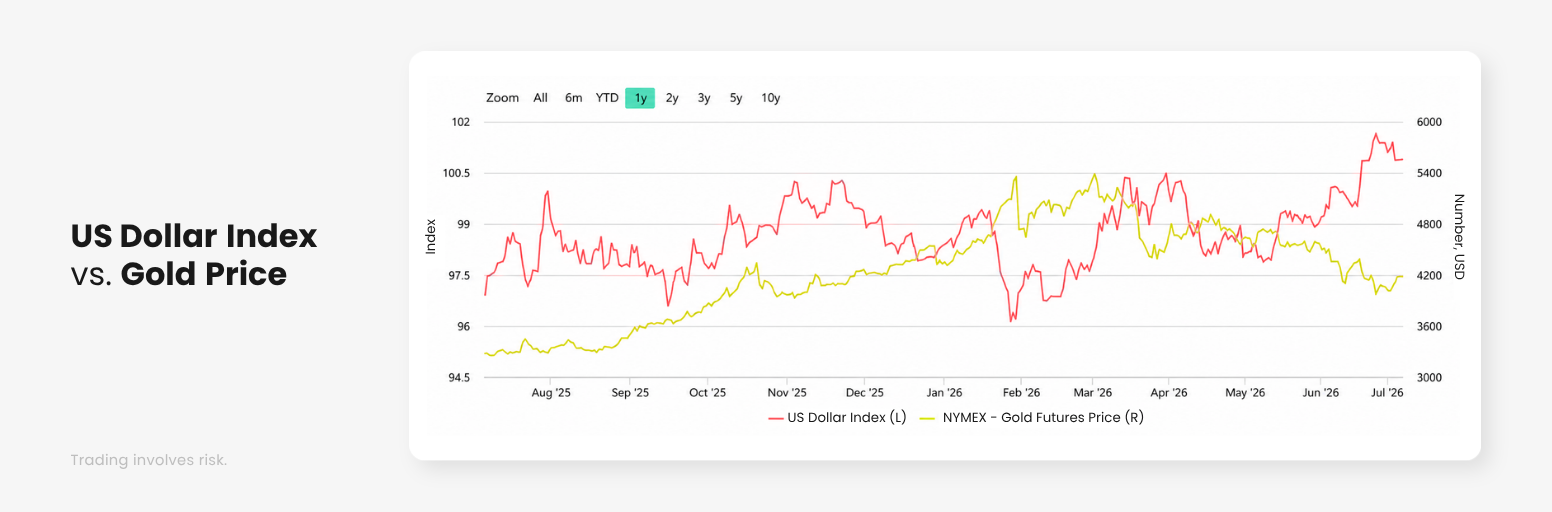

In the first half of 2026, gold failed to extend its upward trend. After reaching a high near USD 5,600, gold prices fell sharply and are now testing the USD 4,000 support level. Prices are already lower than they were at the start of the year.

That has left many traders asking the same question:

If gold is an inflation hedge and safe-haven asset, why is it falling during one of the most uncertain years in recent memory?

The answer is not that gold has lost its role.

The answer is that gold is fighting a stronger opponent: the US dollar.

Last week, D Prime released its “Mid-2026 Macroeconomic Outlook,” noting that the global economy has quietly entered a new Kondratieff cycle. AI is giving markets a long-term reason to stay optimistic, but short-term disruptions remain unavoidable.

The US-Iran war has pushed inflation and rate-hike expectations back into focus. That may continue to pressure asset prices, especially assets that do not generate yield.

Gold sits right at the center of this debate.

So, how could gold perform in the second half of 2026?

Gold Had Every Reason to Rally. So Why Did It Fall?

The first half of 2026 was difficult for gold.

After reaching a high near USD 5,600, prices reversed sharply and are now testing the USD 4,000 support level. Gold is already trading below where it started the year.

In January, prices rose on geopolitical risks and concerns over threats to the Federal Reserve’s independence.

At the end of the month, Donald Trump nominated Kevin Warsh as Fed Chair. Seen as more hawkish, markets priced in tighter policy, and gold quickly pulled back.

In late February, the US-Iran war broke out. Fears of higher inflation and faster rate hikes weighed on precious metals, while some overseas central banks took advantage of high prices to reduce holdings.

Gold continued to fall through March.

In April, easing tensions and lower oil prices briefly improved risk appetite, allowing gold to rebound. But the relief was short-lived.

By late April, stalled US-Iran negotiations and a blocked Strait of Hormuz pushed oil prices higher, putting renewed pressure on gold. During this period, gold and oil showed a clear inverse relationship, as rising oil fueled inflation fears and rate-hike expectations.

The Fed’s April meeting reinforced a hawkish stance, keeping rate-cut expectations low and adding further pressure.

In May, gold traded mostly sideways. Early gains from easing tensions, lower oil prices, and Peru’s energy-related supply disruptions faded quickly, as buying momentum remained weak.

In June, stronger-than-expected US nonfarm payroll data pushed gold lower again. Robust job growth, partly supported by World Cup-related hiring, strengthened confidence in the US economy and lifted rate-hike expectations.

In mid-June, a US-Iran peace framework helped gold rebound briefly. However, the following Fed meeting held rates steady while Chair Warsh signaled a hawkish outlook.

The stronger US dollar once again pressured gold.

Gold’s Biggest Rival Is the US Dollar

This is where the gold story gets interesting.

Gold is still an inflation hedge. Gold is still a safe-haven asset. But it is not the only safe-haven asset in the market.

The US dollar is gold’s biggest competitor.

When the dollar strengthens, global capital often flows into dollar assets instead of gold. Higher inflation, stronger rate-hike expectations, and global uncertainty can all increase demand for the dollar.

That creates a problem for gold.

Gold protects value.

The dollar protects value and pays yield.

When investors can hold dollars and earn higher returns, gold becomes less attractive, especially after a major rally.

This helps explain why gold and crypto have moved more like risk assets this year, rather than behaving like classic safe havens.

Gold is not broken. It is just no longer the only safe-haven trade.

Why AI and Rate-Hike Bets Are Draining Gold Liquidity

Fed rate-hike expectations have pushed capital back into the dollar.

That drains liquidity from gold.

Even if the US-Iran situation eases, inflation comes under control, and the Fed eventually returns to a rate-cut cycle, gold may still struggle to surge immediately.

Normally, when a rate-cut cycle begins, gold benefits first from the liquidity boost. But as risk assets recover, capital may shift away from precious metals and back into stocks, commodities, and other growth-sensitive assets.

In other words, rate cuts may help gold at first, but stronger risk appetite could later limit its upside.

AI is also part of the pressure.

AI is not directly hurting gold. But by keeping US growth alive and attracting capital into stocks, the AI boom is reducing the urgency for rate cuts and pulling liquidity away from precious metals.

US private domestic investment has become the core engine of GDP growth. Capital expenditure from major tech companies is giving the US economy real support.

Even without major additional fiscal stimulus, the US economy can still maintain stable operations.

This has eased some of the market’s earlier concerns about US fiscal sustainability, weakening gold’s medium-term allocation logic.

Gold’s financial attribute is also being suppressed by rate-hike expectations. The root of those expectations is strong economic fundamentals and resilient inflation.

As long as AI sector capex continues to support the economy, the Fed may have less room to cut rates quickly.

That keeps gold under pressure.

High Gold Prices and Russian Supply Add More Pressure

Gold’s previous rally was partly supported by strong central bank buying.

China, Poland, and other central banks are still increasing gold reserves, but rising Russian gold supply may put pressure on the market.

According to a public statement from Russia’s Minister of Natural Resources this month, Russia’s gold output is expected to reach 500 tons in 2025.

That is far above the market’s previous expectation of 350 tons and could make Russia overtake China as the world’s largest gold producer.

Higher supply matters most when demand is already cooling.

With gold prices high, dollar yields attractive, and risk assets recovering, additional Russian output makes it harder for gold to build a strong upside trend.

Overall, current gold price trends are still mainly driven by the macro logic of dollar appreciation.

With high gold prices suppressing demand and Russian output increasing, it is not surprising that gold lacks strong upward momentum.

US Debt Risk Still Supports Gold Long Term

The outlook is not entirely bearish.

Starting in the second half of the year, several factors could shift in gold’s favor.

First, the US dollar may weaken if the US-Iran war eases or ends. For the midterm elections, Trump is actively pushing for peace talks. The dollar index is also already very strong, and strong trends often lose momentum after reaching extreme levels.

Second, central bank gold buying demand remains firm.

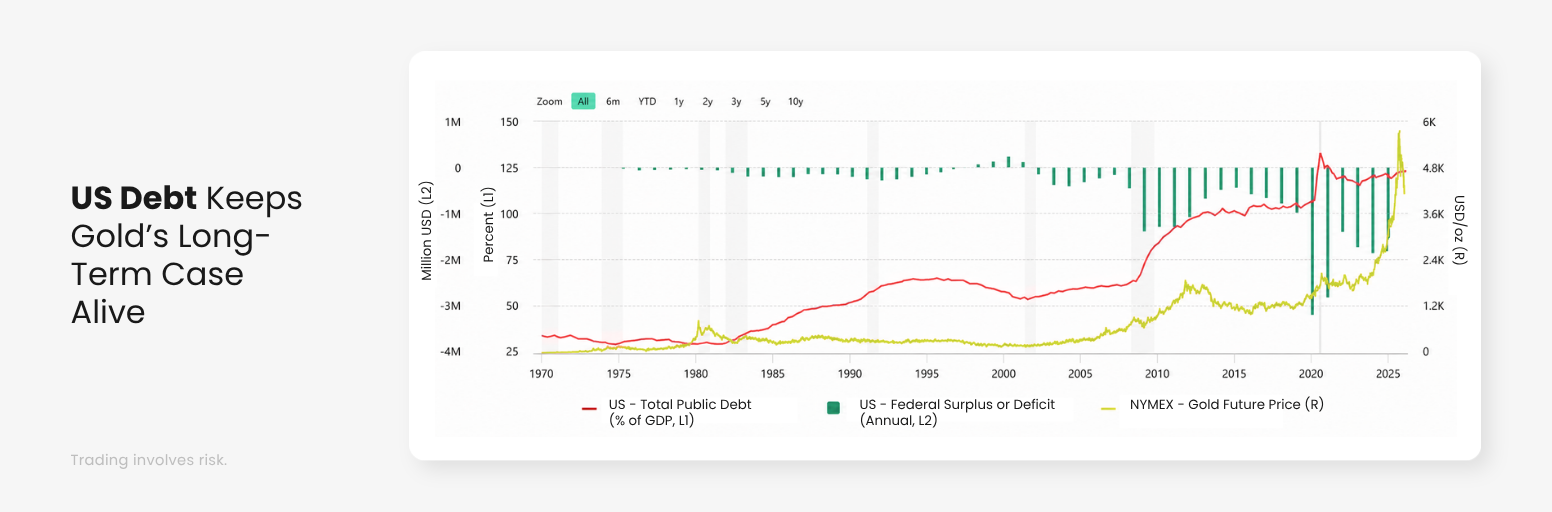

Behind the strong dollar, there is also a deeper fragility that many investors may be underestimating: US debt risk.

Market concerns about dollar credit are rising, mainly because of the continued expansion of US debt and fiscal deficits.

Historically, gold prices have shown a clear positive correlation with total US debt levels. When investors worry more about a US debt crisis, safe-haven demand for gold tends to increase.

Current US debt levels are already at a record high.

According to data released by the US Congressional Budget Office in February 2026, the US national debt-to-GDP ratio is expected to rise from 99.4% to 120.2% by 2035.

On May 16, 2025, Moody’s officially downgraded the US long-term sovereign credit rating from Aaa to Aa1. This reflected growing market concern over US fiscal sustainability.

The total size of US interest-bearing national debt has now exceeded the historical peak of USD 39 trillion.

The CBO also predicts that US annual net interest payments on debt will exceed USD 1 trillion every year for the next decade.

This creates a major policy dilemma.

A huge debt burden could force the Fed to tilt monetary policy toward “serving fiscal needs.” Over time, the pressure to maintain lower interest rates may increase.

As long as US debt expansion is not fundamentally reversed, gold still has room to rise as a hedge against dollar credit risk.

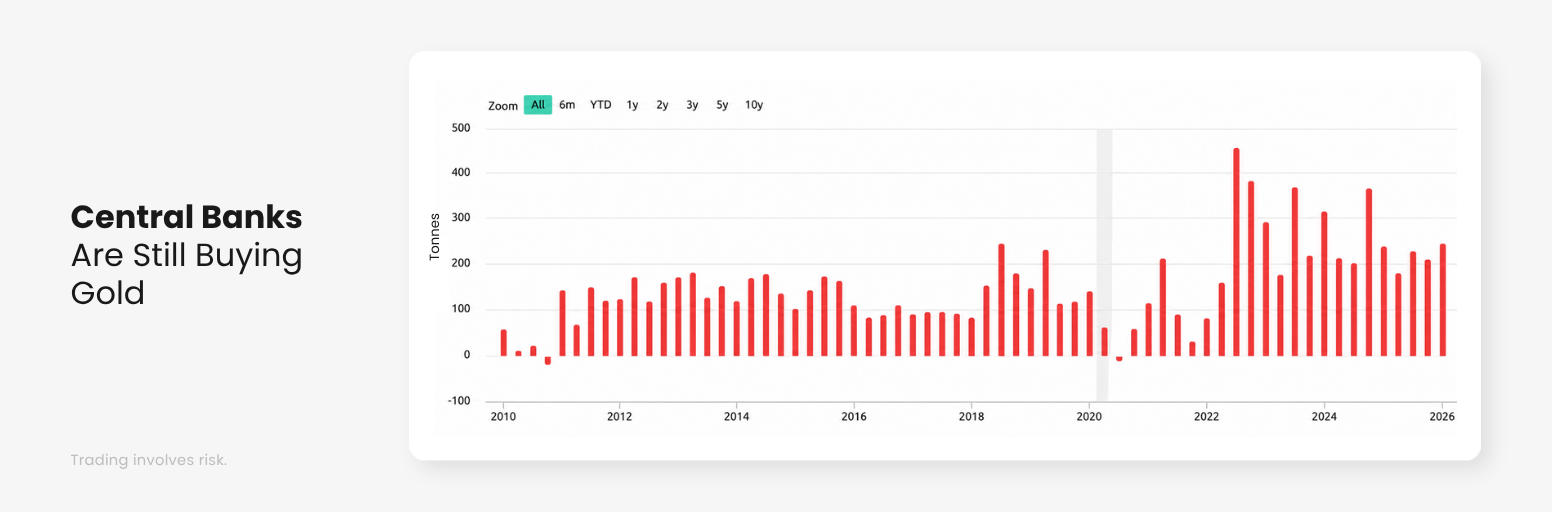

Central Banks Are Still Buying Gold

Global central bank demand for gold remains strong.

For many emerging market countries, increasing gold reserves is an effective way to hedge against dollar credit risk.

In recent years, global central bank gold purchases have remained high, and willingness to increase holdings continues to rise.

In the third quarter of 2022, global central bank quarterly gold purchases reached a record high of 456.9 tons. Since then, overall buying volumes have stayed elevated.

Total gold purchases in 2025 were about 850 tons.

In the first quarter of 2026, central bank gold purchases reached 243.7 tons, continuing the strong trend.

Poland, Uzbekistan, Kazakhstan, and China increased their gold holdings by 31.43 tons, 25.19 tons, 12.55 tons, and 7.15 tons, respectively.

However, some countries reduced their holdings. Turkey sold 79.45 tons, while Russia sold 21.77 tons.

At first glance, that may look negative for gold. But the bigger picture is more balanced.

According to the World Gold Council’s 2025 Global Central Bank Gold Reserve Survey, 95% of surveyed central banks believe the global central bank gold buying trend will continue over the next 12 months.

The key point is simple: central banks are not abandoning gold.

Some selling looks tactical, while long-term reserve diversification remains intact.

Why Turkey, Russia and China Matter for Gold Demand

Many investors worry that gold selling by Turkey and Russia could pressure gold prices.

But the impact may be limited.

Turkey’s 79-ton gold reduction in the first quarter was mostly concentrated in March. This appears to have been a short-term liquidity operation rather than a long-term shift away from gold.

Turkey later added 36.4 tons of gold back to its reserves in the following two weeks.

Russia’s gold selling was also driven by specific domestic pressures.

Falling energy revenues increased fiscal pressure, and gold selling was used to support finance ministry asset liquidation and smooth potential fluctuations in the ruble exchange rate and market liquidity.

This does not look like a sustainable long-term selling trend.

China’s gold reserve accumulation is still moving forward.

When gold prices corrected in March and April 2026, China’s buying pace accelerated significantly.

From January to April 2026, China’s monthly gold purchase volumes were:

- January: 1.24 tons

- February: 0.93 tons

- March: 4.98 tons

- April: 8.09 tons

As of April 2026, China had increased its gold holdings for 18 consecutive months.

This steady buying is important because it reflects continued demand for gold as a long-term reserve asset.

Gold Outlook for H2 2026: Range-Bound, Not Broken

Gold is now caught between two forces.

On one side, upside is being capped by a strong dollar, high yields, AI-driven risk appetite, rising Russian supply, and Fed rate-hike expectations.

On the other side, downside is being supported by central bank buying, US debt risk, potential dollar weakness, and gold’s long-term role as a hedge against inflation and dollar credit risk.

That creates a market with both upward resistance and downward support.

Gold may not be ready for a strong one-way rally in the second half of 2026.

But it is also not broken.

The more likely scenario is that gold continues to trade in a broad range, supported by long-term structural demand but capped by stronger competing assets.

Gold Is Still a Hedge, Just Not the Main Trade

Gold’s problem in 2026 is not that it has lost its safe-haven role.

Its problem is that the market has another safe haven with yield: the US dollar.

As long as the dollar stays strong and rate-hike expectations remain alive, gold may struggle to break higher.

But if the US-Iran conflict eases, the dollar weakens, and investors refocus on US debt risk, gold could find stronger support again.

For traders, the key is not to treat gold as a simple “war goes up, peace goes down” asset.

Gold is being pulled by three forces at the same time:

- Dollar strength

- Central bank demand

- US debt and inflation risk

That means gold may stay range-bound in the second half of 2026, but it remains one of the most important assets to watch.

In this market, gold is not the main character.

But it is still very much in the story.

By D Prime Analysis Team

Macro and market strategy research by D Prime’s in-house analysis team.

Risk Disclosure

Trading in Securities, Futures, contracts for difference (CFDs) and other financial products carries high risks due to the rapid and unpredictable fluctuation in the value and prices of these financial instruments. This unpredictability is due to the adverse and unpredictable market movements, geopolitical events, economic data releases, and other unforeseen circumstances. You may sustain substantial losses, including losses exceeding your initial investment within a short period of time.

You are strongly advised to fully understand the nature and inherent risks of trading with the respective financial instrument before engaging in any transactions with D Prime. When you engage in transactions with us, you acknowledge that you are aware of and accept these risks.

Disclaimer

The information contained herein is provided for general informational and educational purposes only and does not constitute investment advice, financial advice, trading advice or any other form of professional advice, a recommendation, or an offer or solicitation to buy or sell any financial instruments or engage in any trading strategy.

Trading in leveraged products such as contracts for difference (CFDs) involves a significant risk of loss and may not be suitable for all investors. Past performance is not indicative of future results. Any references to market trends, asset performance, price levels, or forward-looking statements reflect opinions or general market commentary as at the date of publication and are subject to change without notice.

This article does not take into account any individual investor’s objectives, financial situation, or risk tolerance. Readers should conduct their own independent research and seek professional advice before making any investment or trading decisions. D Prime and its affiliates make no representations or warranties about the accuracy or completeness or reliability of this information and disclaim any and all liability for any direct, indirect, incidental, consequential, or other losses or damages arising out of or in connection with the use of or reliance on any information contained herein. The above information should not be used or considered as the basis for any trading decisions or as an invitation to engage in any transaction. Do not rely on this article to replace your independent judgment.

“D Prime” is a brand name of D Prime Vanuatu Limited, a company incorporated and regulated by the Vanuatu Financial Services Commission (Company Number: 700238). The availability of products and services may vary depending on jurisdiction and applicable regulatory requirements.