Just weeks ago, the market narrative was simple.

Inflation was cooling.

The Fed was preparing to cut rates.

A soft landing looked achievable.

Then the US–Iran conflict escalated.

And almost overnight, that narrative broke.

D Prime hosted a live session on April 2, bringing together top traders from the #DooTrader Island Showdown finals in Bali, alongside financial KOL AlgoChadLin, who has over 300,000 followers in China.

His talk focused on three critical questions:

- Where was the economy before the war?

- Will inflation return, and how will assets move?

- How might the US–Iran conflict end?

1. Before the War: A Recovery Hiding in Plain Sight

At first glance, the US economy looked weak.

But beneath the surface, it was already recovering.

A Quiet Recovery Driven by AI

This recovery is being supported by a new AI-driven productivity cycle.

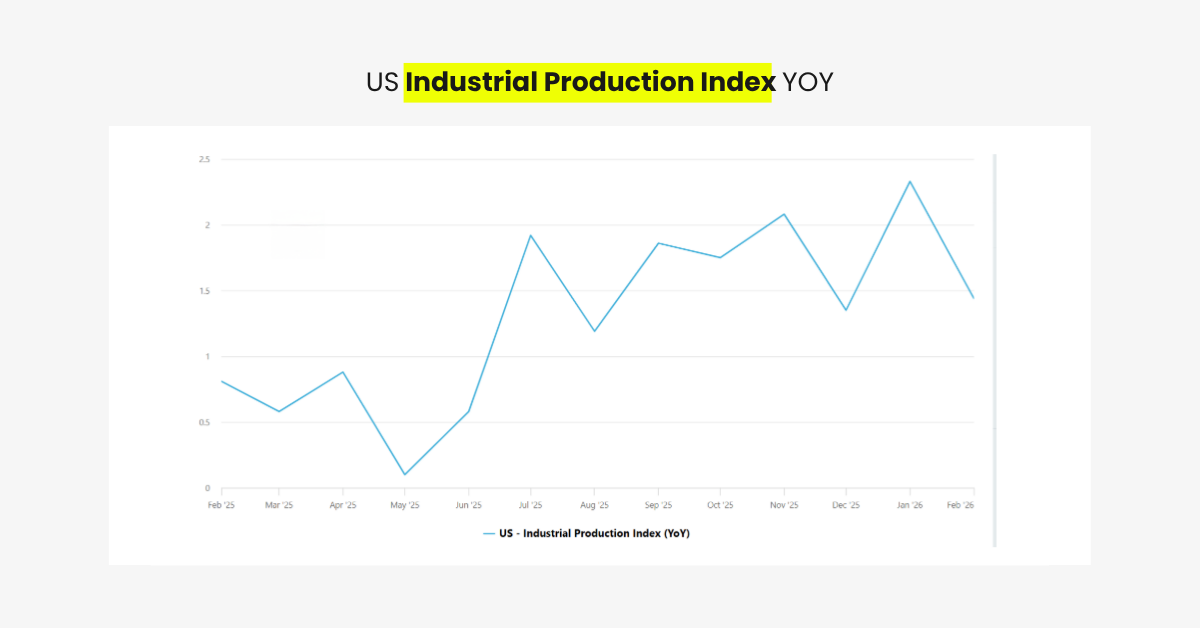

- US industrial production rose 0.2% in February

- Following 0.7% growth in January

- Marking the fourth consecutive month of expansion

- ISM PMI beat expectations

Demand for AI computing power is becoming a structural driver of industrial growth.

Demand Remains Weak — But Not Broken

At the same time, consumption remains fragile.

- Retail sales fell -0.16% in January

- Slightly better than the expected -0.3%

The decline was mainly driven by:

- dining

- auto sales

Even without the war, demand faces pressure from:

- tariffs

- inflation

- weak employment

However, upcoming tax rebates from the “One Big Beautiful Bill Act” may provide support.

Consumption is not strong but it is also not collapsing.

The Labor Market Is Changing, Not Crashing

February employment data surprised markets:

- Nonfarm payrolls dropped 92,000 (vs +55,000 expected)

- Unemployment rose to 4.4% (vs 4.3% expected)

At first glance, this looks concerning.

But the details matter.

Weakness is concentrated in:

- healthcare

- IT

- professional services

These are sectors being reshaped by AI and automation.

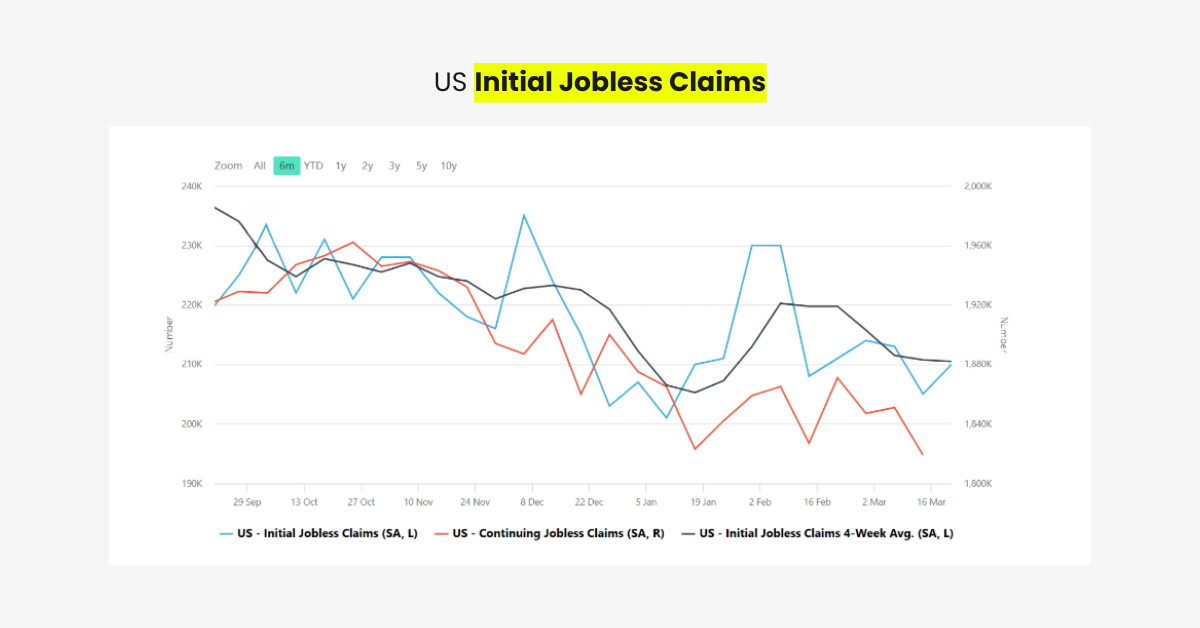

Meanwhile:

- Initial jobless claims have not surged

- Suggesting February may represent a temporary low point

This is not a traditional downturn.

It is a structural adjustment.

Then the Market Shifted Focus

All of this data reflects conditions before the war escalated.

Once tensions rose, markets stopped focusing on growth.

They shifted entirely to one variable:

inflation.

2. Inflation and Asset Outlook

Inflation Was Already Rising

The key insight is this:

Inflation did not start with the war.

It was already building.

- PPI rose 0.7% month over month

- Above the previous 0.5% and expected 0.3%

- Year-over-year PPI reached 3.37% (vs 2.9% expected)

The war is not the cause.

It is the accelerator.

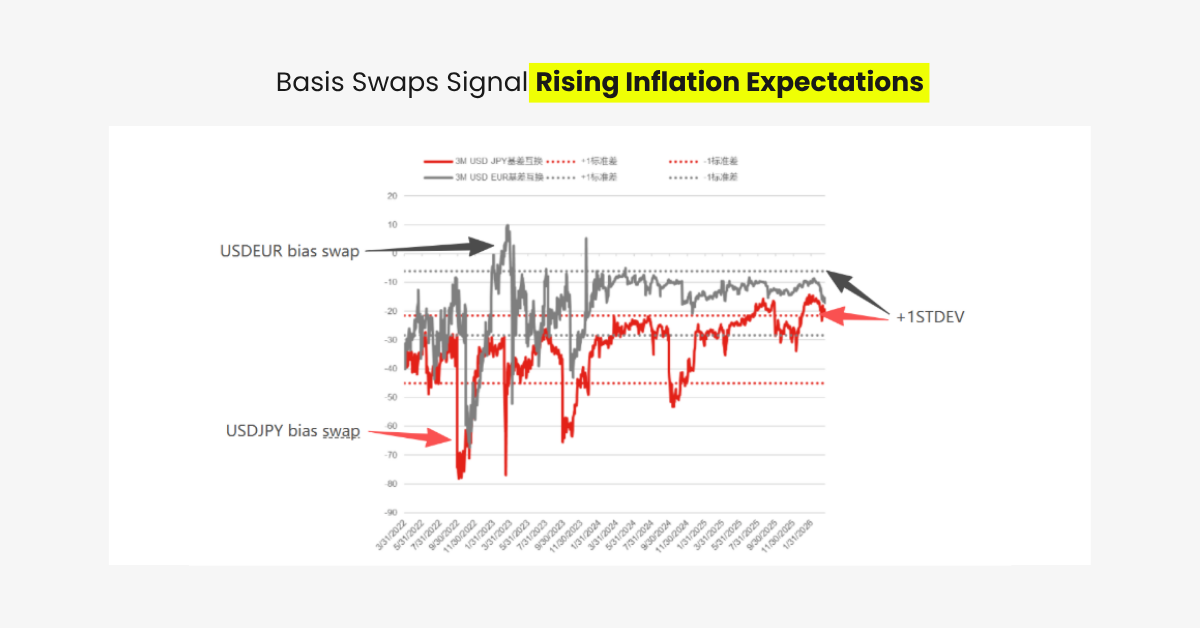

Short Term: Inflation Is Already Priced In

Markets have reacted aggressively.

- FX basis swaps in USDJPY and EURUSD moved beyond one standard deviation

- Strong positioning for a stronger dollar

This suggests inflation expectations are already reflected in asset prices.

Even upcoming CPI releases may have limited surprise impact.

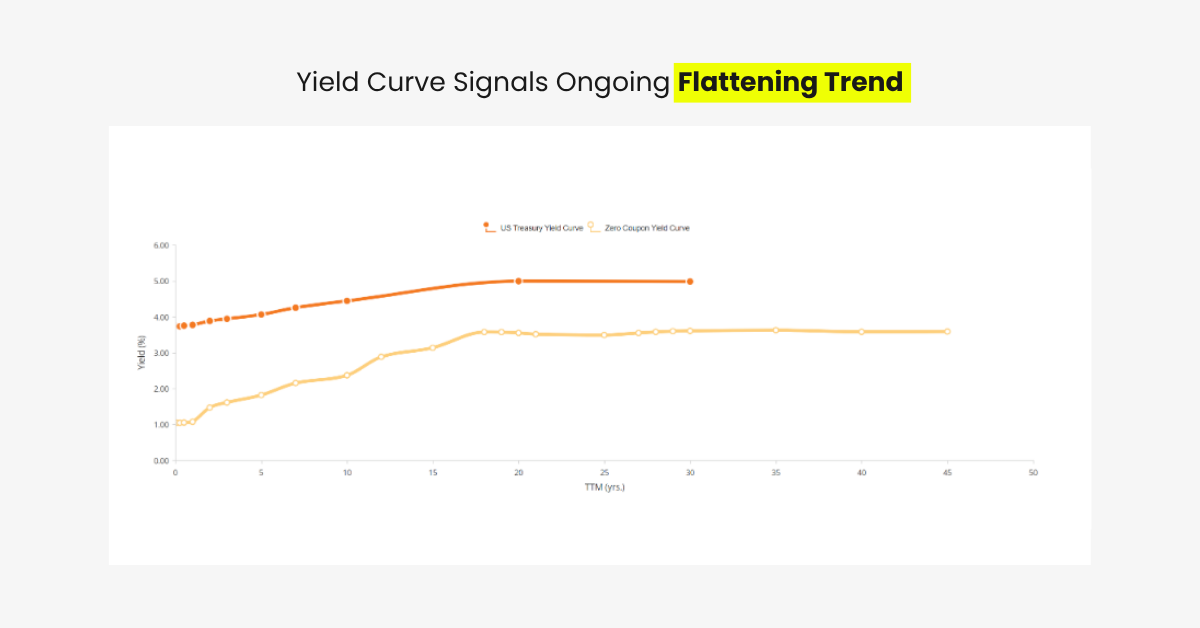

Medium Term: The Yield Curve Is Sending a Warning

The yield curve is flattening.

- Short-term yields are rising

- Long-term yields remain capped

This reflects two forces:

- inflation expectations increasing

- recession fears building

A flattening curve is often a signal that markets are preparing for a downturn.

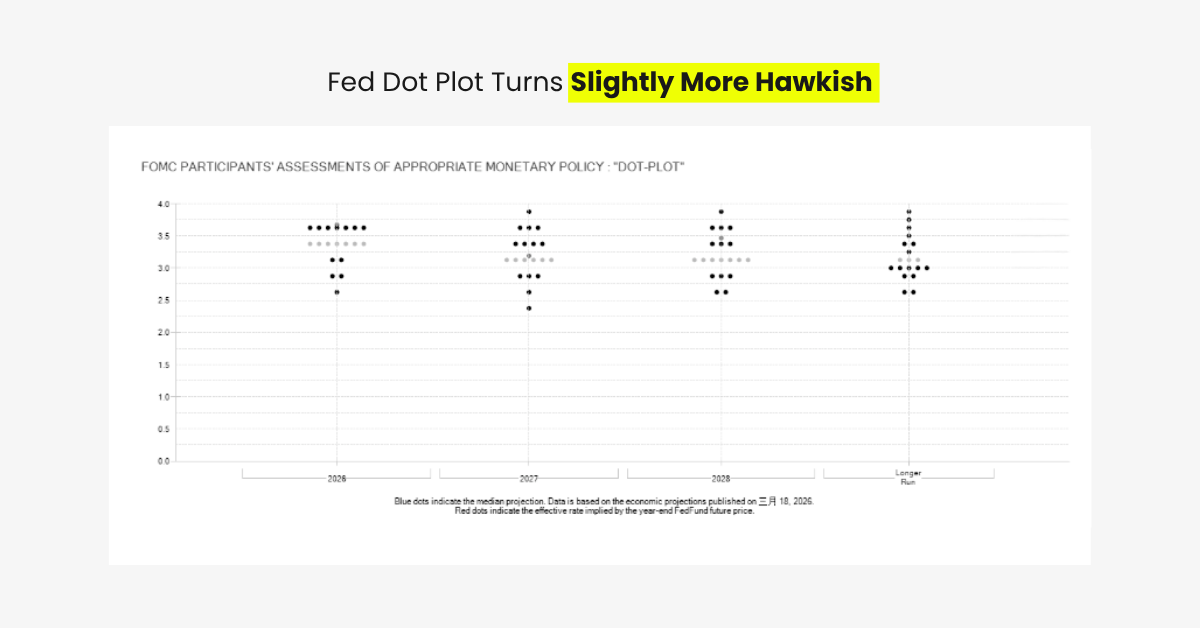

Are Rate Hikes Coming Back?

Markets are starting to price in rate hikes.

But this may be too pessimistic.

- The Fed’s dot plot still suggests one rate cut this year

- Interest rates are already high

- The labor market remains fragile

Aggressive tightening in this environment could damage growth further.

Asset Performance: A Market in Transition

With inflation and recession risks largely priced in, markets are repositioning:

Equities

- Most vulnerable to stagflation

- S&P 500 has fallen for four consecutive weeks

- Tech stocks are under pressure

US Treasuries

- Yield curve flattening

- Signals potential recession within 12–18 months

Gold

- Underperforming despite uncertainty

- A stronger dollar is pulling capital away

FX Markets

- Dollar strength is dominant

- USDJPY ↑

- USDCAD ↑

- EURUSD ↓

- GBPUSD ↓

3. How Will the War End?

This is the most uncertain part of the equation.

And it is where markets are most sensitive.

Oil Is the Real Weapon

The key insight is clear:

Iran’s strongest weapon is oil.

Supply disruptions across the region are significant:

- Iraq

- Qatar

- Kuwait

- Saudi Arabia

Combined cuts exceed 10 million barrels per day.

This keeps oil prices above $100 per barrel.

And keeps inflation pressure alive.

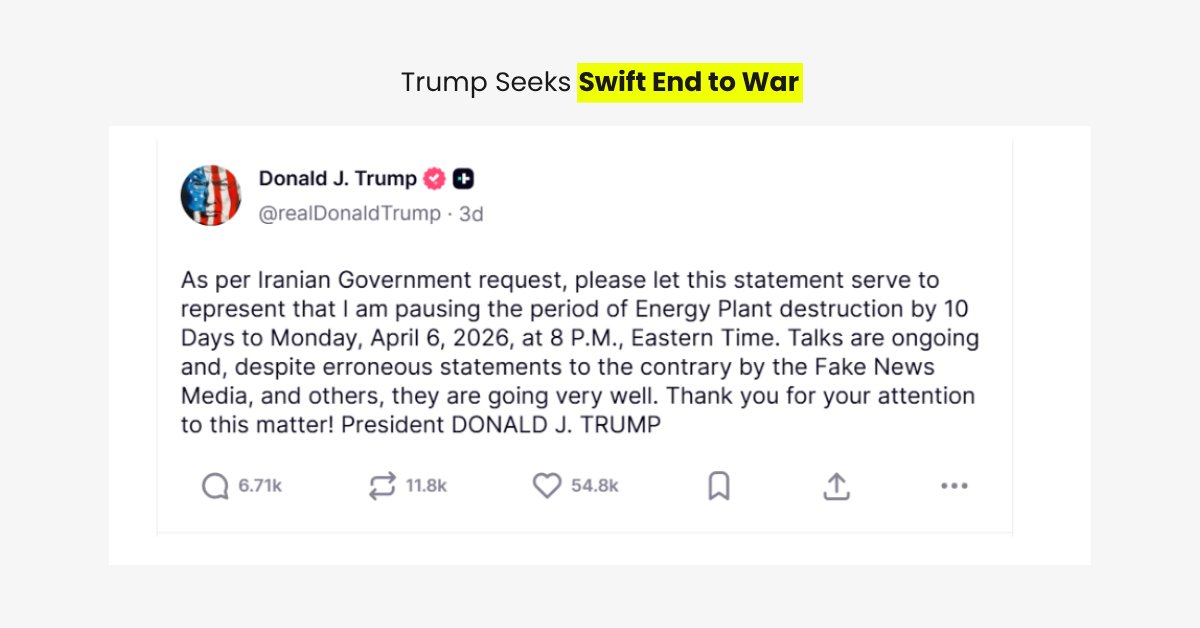

Economic Pressure Is Turning Political

The impact is no longer just economic.

It is political.

- inflation rising

- equities falling

- voter pressure increasing

Recent signals suggest the US may be exploring de-escalation options.

Three Possible Scenarios

Scenario 1: Quick Resolution (Within 1 Month)

- Oil prices fall rapidly

- Strategic reserves and OPEC stabilize supply

Scenario 2: Controlled Conflict (2–3 Months)

- Oil remains above $100

- Supply disruptions persist

Scenario 3: Prolonged Conflict (6+ Months)

- Global energy crisis

- High probability of stagflation and recession

What This Means for Markets

The market is entering a new phase.

Not a clean recovery.

Not a full downturn.

But a transition.

- Inflation is returning

- Growth is uneven

- Policy flexibility is shrinking

This is where volatility increases.

And positioning becomes critical.

Ultimately, a de-escalation would benefit not just markets, but the broader global economy.

Disclaimer

The information contained herein is provided for general informational and educational purposes only and does not constitute investment advice, financial advice, trading advice, or any other form of professional advice. Nothing contained herein should be construed as a recommendation, endorsement, offer, or solicitation to buy or sell any financial instruments or to engage in any investment or trading strategy.

The content provided, including but not limited to data, analyses, market commentary, price levels, and forward-looking statements, reflects general market opinions based on publicly available information. Such information may be subject to change, revision, or update at any time without prior notice.

This article does not take into account any individual investor’s objectives, financial situation, or risk tolerance. Readers should conduct their own independent research and seek professional advice before making any investment or trading decisions. D Prime and its affiliates make no representations or warranties about the accuracy or completeness or reliability of this information and disclaim any and all liability for any direct, indirect, incidental, consequential, or other losses or damages arising out of or in connection with the use of or reliance on any information contained herein. The above information should not be used or considered as the basis for any trading decisions or as an invitation to engage in any transaction. Do not rely on this article to replace your independent judgment.

“D Prime” is a brand name of D Prime Vanuatu Limited, a company incorporated and regulated by the Vanuatu Financial Services Commission (Company Number: 700238). The availability of products and services may vary depending on jurisdiction and applicable regulatory requirements.